Not every financial advisor operates the same way. That misconception costs clients money, limits advisors' potential, and blurs one of the most meaningful distinctions in the industry. The independent advisor service model, formally anchored in the Registered Investment Advisor (RIA) framework, represents a fundamentally different way of delivering financial advice. It changes who the advisor works for, how they get paid, what products they can recommend, and how much control they have over their own practice. Whether you are considering going independent or evaluating your options as a client, understanding this model gives you a real advantage.

Table of Contents

- Key Takeaways

- What is the independent advisor service model

- Independent model vs. wirehouse and broker-dealer models

- Benefits and challenges of operating independently

- Building a strong independent advisor value proposition

- Practical steps for transitioning to the independent model

- My honest take on independence after years in this space

- Grow your independent practice with Mastermindadvisormarketing

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Independence has a legal definition | The RIA framework and fiduciary standard form the legal backbone of the independent advisor service model. |

| Compensation differs significantly | Independent advisors retain up to 85% of revenues compared to 35-50% at traditional wirehouse firms. |

| Fiduciary duty is ongoing | RIAs must act in the client's best interest 100% of the time, not just at the point of sale. |

| Operational demands are real | Running an independent practice means owning compliance, technology, and client service infrastructure. |

| Value proposition depends on transparency | Documenting recommendations and showing clients real alternatives builds lasting trust and loyalty. |

What is the independent advisor service model

The independent advisor service model is a practice structure where a financial advisor operates outside the direct employment of a large bank, wirehouse, or captive insurance company. Instead, the advisor typically registers as a Registered Investment Advisor (RIA) with the SEC or their state securities regulator, placing them under a fiduciary standard that legally requires them to put client interests first at all times.

This is not just a title. The RIA model emphasizes transparent pricing, open investment access, and fiduciary duty as core operational features. Those three elements shape everything from how the advisor charges for services to which investments they can recommend and how they disclose potential conflicts.

The model has several defining characteristics worth knowing:

- Fiduciary standard. The advisor is legally obligated to act in your best interest, not just recommend products that are "suitable."

- Open architecture. Independent advisors are not restricted to a proprietary product shelf. They can access third-party funds, ETFs, and strategies from across the market.

- Ownership of client relationships. The advisor, not the firm, owns the book of business. If they move or close, they take their clients with them.

- Fee transparency. Compensation is typically disclosed upfront through fee schedules, whether asset-based, flat retainer, or hourly.

- Business autonomy. The advisor controls their brand, service model, and client experience without corporate mandates dictating how they operate.

Understanding these features helps both clients and advisors recognize what true independence actually delivers, rather than accepting a label at face value.

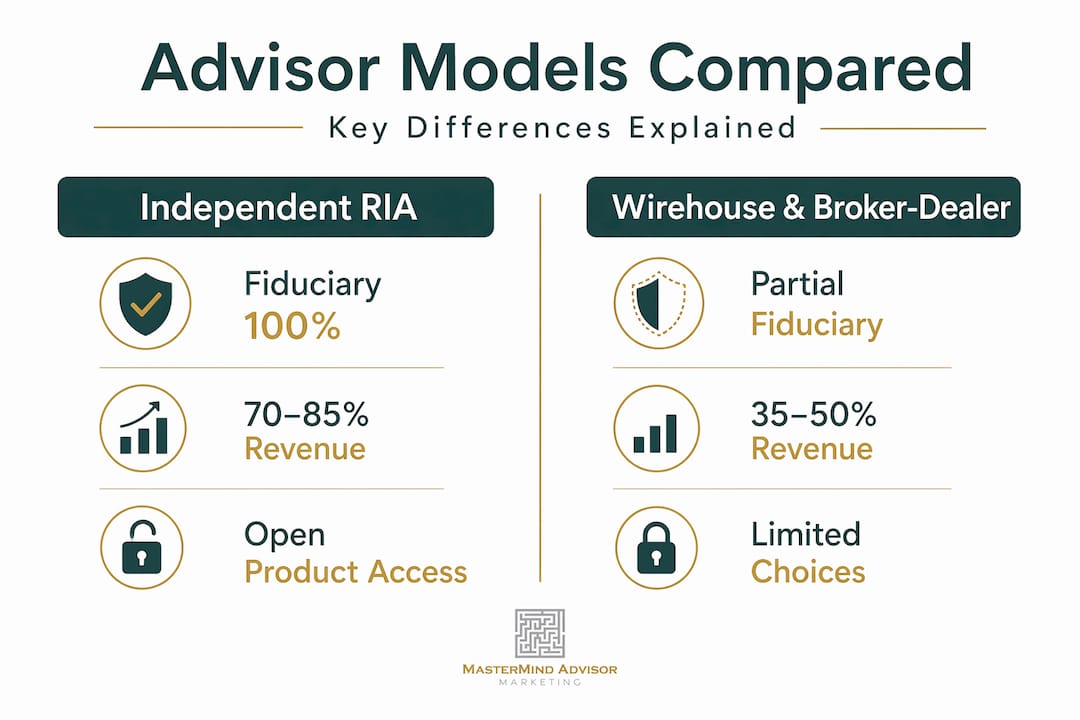

Independent model vs. wirehouse and broker-dealer models

The sharpest way to understand the independent advisor business model is to compare it directly to the two dominant alternatives: the wirehouse model and the broker-dealer model.

| Feature | Independent RIA | Wirehouse | Broker-Dealer |

|---|---|---|---|

| Fiduciary standard | Yes, 100% of the time | No | Regulation Best Interest only |

| Revenue payout | 70-85% to advisor | 35-50% to advisor | Varies by agreement |

| Product access | Open architecture | Proprietary shelf priority | Partially open |

| Client relationship ownership | Advisor-owned | Firm-owned | Often firm-owned |

| Brand control | Full | None | Partial |

| Compliance responsibility | Advisor-managed | Firm-managed | Shared |

Independent advisors retain up to 70-85% of revenues versus 35-50% at wirehouses and gain substantially more product choice. That payout difference is not just a financial benefit. It reflects who the practice actually belongs to.

On the regulatory side, RIAs are fiduciaries 100% of the time, unlike broker-dealers who fall under Regulation Best Interest (Reg BI), a narrower standard that applies primarily at the point of a recommendation rather than throughout the client relationship. That distinction matters when a client's financial situation changes and ongoing advice is needed.

Pro Tip: If you are evaluating whether to go independent, ask your current firm directly: "Do you own my client list?" The answer will tell you more about your situation than any contract review.

The trade-off is real, though. Wirehouse advisors benefit from institutional infrastructure, compliance departments, technology platforms, and marketing support, all included. Independent advisors give that up in exchange for control and economics. Neither path is inherently superior. The right choice depends on the advisor's business goals, risk tolerance, and service philosophy.

Benefits and challenges of operating independently

The advantages of the independent advisory services model are compelling, but they come with conditions attached.

On the upside, the benefits are substantial:

- Higher earning potential. The revenue payout math alone makes independence attractive for advisors with an established client base.

- Fee structure flexibility. Advisors can offer AUM-based fees, flat retainers, hourly rates, or hybrid models without approval from a corporate compliance department.

- Deeper client trust. Open fee disclosure builds stronger client relationships. Clients who understand exactly what they pay and why tend to stay longer and refer more often.

- Service customization. Without corporate mandates, advisors tailor the client experience around what clients actually need rather than what the firm sells.

- Practice value. Because the advisor owns the client relationships, the practice itself has real equity value that can be sold, merged, or passed on.

The challenges are equally real. Independent advisors must manage compliance, vendor integrations, and client service infrastructure themselves. That means hiring or outsourcing compliance support, selecting and paying for a custodian, building or licensing technology for portfolio management, CRM, and financial planning, and handling everything from data security to marketing strategy.

Pro Tip: Before transitioning to independence, map out your full operating budget including technology, compliance, office, and insurance costs. Many advisors underestimate total overhead by 20-30%, which affects how quickly the economics actually improve.

Some advisors explore partial independence models such as captive RIAs or Independent Broker-Dealers. These can offer some freedom, but some "independent" models still restrict product menus and innovation despite branding freedom. Real independence means control over the full practice, not just the logo on the door.

Building a strong independent advisor value proposition

The independent advisor value proposition is not automatic. It has to be built deliberately and communicated clearly. Here is how advisors operating under this model turn their structure into a genuine competitive advantage:

-

Document your rationale. Written client rationale showing explicit alternatives and tradeoffs closes the information gap that erodes trust in traditional models. When a client sees that you considered three strategies and chose one for specific reasons tied to their goals, they stop wondering whether you are selling them something.

-

Create a client-centric service experience. Independent advisors are not constrained by product quotas or scripted service standards. Use that freedom intentionally. Define your ideal client, design your service calendar around their needs, and make every touchpoint feel personal rather than transactional.

-

Leverage educational marketing. Educational content and testimonials help independent advisors communicate their unique value in a market where most consumers cannot tell a fiduciary from a salesperson. Content that explains how your fee structure works or what fiduciary duty actually means for clients does two things at once: it educates and it differentiates.

-

Use technology to personalize communication. CRM systems, automated follow-ups, and segmented email campaigns let independent advisors maintain the feel of a personal relationship at scale. Clients who hear from you consistently trust you more, even if each individual contact is brief.

-

Be explicit about what you do not do. One of the clearest signals of independence is telling clients what you will not recommend and why. That kind of transparency is rare enough that it stands out immediately.

A well-built independent advisor value proposition does not just say "I work for you." It proves it through every interaction, document, and conversation. You can also explore how advisor podcasts have become a powerful way to demonstrate expertise and build authentic client trust at scale.

Practical steps for transitioning to the independent model

If you are seriously considering the move, the planning process matters as much as the decision itself. Here is what that preparation actually looks like:

- Audit your current agreements. Non-solicitation and non-compete clauses vary widely. Know exactly what your current firm allows before you say anything to clients or colleagues.

- Select a custodian early. Your custodian holds client assets and forms the operational backbone of your RIA. Major options each have different minimum asset requirements, technology integrations, and service models. Evaluate them on all three dimensions.

- Build your technology stack before launch. Portfolio management software, financial planning tools, a CRM, and secure document sharing are not optional. Trying to piece these together after going live creates gaps that clients notice.

- Establish a compliance framework. Whether you hire a Chief Compliance Officer or outsource to a compliance firm, you need written policies and procedures in place before you register. The SEC and state regulators will ask for them.

- Develop your marketing strategy in parallel. Many advisors focus entirely on operations and launch with no system for client education or prospect engagement. That slows growth significantly in the first year.

The types of independent advisor service packages you offer should also be mapped out before launch. Whether you charge a flat annual retainer for comprehensive planning or percentage-based fees for portfolio management, clarity on your service tiers makes onboarding smoother and reduces pricing objections.

My honest take on independence after years in this space

I have watched hundreds of advisors debate independence, and I can tell you the ones who thrive and the ones who struggle usually split on one factor: whether they treated independence as an operational decision or just a label.

The advisors who treat it as a label think that registering as an RIA and printing new business cards is enough. They assume clients will immediately understand and appreciate the difference. They almost always get a rude awakening. The fiduciary story does not sell itself. You have to tell it, prove it, and repeat it constantly.

The ones who treat it as an operational commitment build real infrastructure. They put transparency at the center of every client conversation. They document why they make specific recommendations. They have a marketing system that actually communicates what independence means and why it matters to the people they serve.

What I have also found is that many advisors underestimate the backend demands of running a fully independent firm. Compliance is not a one-time box to check. Technology costs compound over time. And without a system for generating new clients, even a successful transition can stall. The advisors I respect most planned for all of this before they made the move, not after.

The future of advisor independence is bright, but only for those who show their work. Clients are getting more sophisticated. Transparency is becoming a baseline expectation, not a differentiator. The advisors who document their process, educate their clients, and run their practice like a real business will win. The rest will wish they had started sooner.

— Josh

Grow your independent practice with Mastermindadvisormarketing

Building an independent advisory practice is one thing. Getting in front of the right prospects and keeping your pipeline full is another challenge entirely. Mastermindadvisormarketing was built specifically for this problem. The platform gives independent financial advisors a turnkey system of custom webinars, seminars, and content marketing that turns your fiduciary story into real client relationships. Automated follow-ups and a custom CRM keep you visible without requiring constant manual effort. If you are ready to put your independent advisor value proposition to work in the market, explore the platform and see what advisors who have already made the leap are doing to grow.

FAQ

What is the independent advisor service model?

The independent advisor service model is a practice structure where a financial advisor operates as a Registered Investment Advisor (RIA), bound by fiduciary duty, with open product access and full ownership of their client relationships outside of a wirehouse or captive firm.

How does the independent advisor model differ from a broker-dealer?

RIAs are fiduciaries 100% of the time, while broker-dealers operate under Regulation Best Interest, which applies a narrower standard only at the point of a recommendation rather than throughout the ongoing client relationship.

What are the main benefits of going independent?

Independent advisors typically retain 70-85% of revenues, gain full control over their service model and product access, and can offer greater fee transparency, which builds deeper client trust over time.

What challenges do independent advisors face?

The biggest challenges are managing compliance, selecting and paying for technology and custodial services, and building a client acquisition system without the institutional marketing support that larger firms provide.

How do independent advisors build their value proposition?

By documenting the rationale behind recommendations, disclosing fees clearly, using educational content to explain the fiduciary difference, and leveraging tools like client testimonials to communicate their unique value to prospects.