A review strategy for financial advisors is a systematic approach to gathering, managing, and leveraging client testimonials and feedback to build trust, increase visibility, and grow a practice. Understanding why advisors need review strategy is no longer optional. 83% of consumers want documented credibility like reviews before hiring a financial advisor, and 25% of affluent Americans now use AI tools to find advisors, with reviews as a primary signal. The industry term for this practice is "reputation management," but in financial services, it carries a compliance dimension that makes it uniquely demanding and uniquely rewarding.

Why advisors need a review strategy to grow in 2026

A structured review strategy directly improves both client retention and new prospect acquisition. Advisors with systematic review programs see 40–60% higher conversion on inbound prospects within 12–24 months, driven by social proof and improved search rankings. That gap is not marginal. It represents the difference between a practice that grows on referrals alone and one that compounds growth through digital visibility.

Social proof closes the trust gap faster than any brochure or cold outreach. When a prospect searches for a financial advisor and finds a profile with recent, specific reviews, they arrive at the first conversation already partially convinced. Reviews also feed local search algorithms and AI recommendation engines, which increasingly surface advisors based on review velocity and sentiment rather than just credentials.

The role of client testimonials extends beyond marketing. Testimonials signal to existing clients that their peers value the relationship, which reinforces loyalty. Advisors who treat reviews as a growth system rather than a one-time marketing task consistently outperform those who rely on passive word-of-mouth.

Key benefits of a structured review approach include:

- Higher inbound conversion rates driven by social proof at the top of the prospect funnel

- Improved local SEO and AI discovery as review velocity signals relevance to search engines

- Stronger client retention because the review request process itself deepens the advisor-client relationship

- First-mover advantage since only 10–15% of RIAs actively leverage testimonials today

That last point deserves emphasis. The advisors who build review programs now will own the digital reputation space before the majority of their peers catch up.

What makes review collection uniquely hard for financial advisors?

Financial advisory has no natural finish line. A dentist completes a procedure. A tax preparer files a return. A financial advisor's work is continuous, which means there is no obvious moment to say, "We just finished something great. Would you leave us a review?" Advisors must tie review requests to ongoing relationship touchpoints like annual planning meetings to maintain consistency.

This structural challenge creates three specific problems:

- Timing ambiguity. Without a clear service endpoint, advisors either ask too early (before the client feels real value) or too late (after the moment of peak satisfaction has passed).

- Compliance risk. The SEC Marketing Rule governs how advisors solicit and display testimonials. A poorly worded review request or an undisclosed incentive can trigger regulatory scrutiny.

- Relationship sensitivity. Asking a long-term client for a review can feel transactional if the request is not framed around the relationship rather than the advisor's marketing needs.

Operational compliance gaps often arise from failing to record the solicitation process and required disclosures, not just the review content itself. That means the risk is not only in what a client writes but in how the advisor asked.

Pro Tip: Ask for reviews at low-stress, high-value moments. Tax check-ins, year-end planning calls, and milestone conversations (retirement date confirmed, college funding complete) are natural openings. Clients feel good at those moments, and the request feels like a logical extension of the conversation rather than an interruption.

The relationship-driven nature of financial advisory is actually an asset once you recognize it. You have more high-value touchpoints than almost any other profession. The challenge is learning to use them.

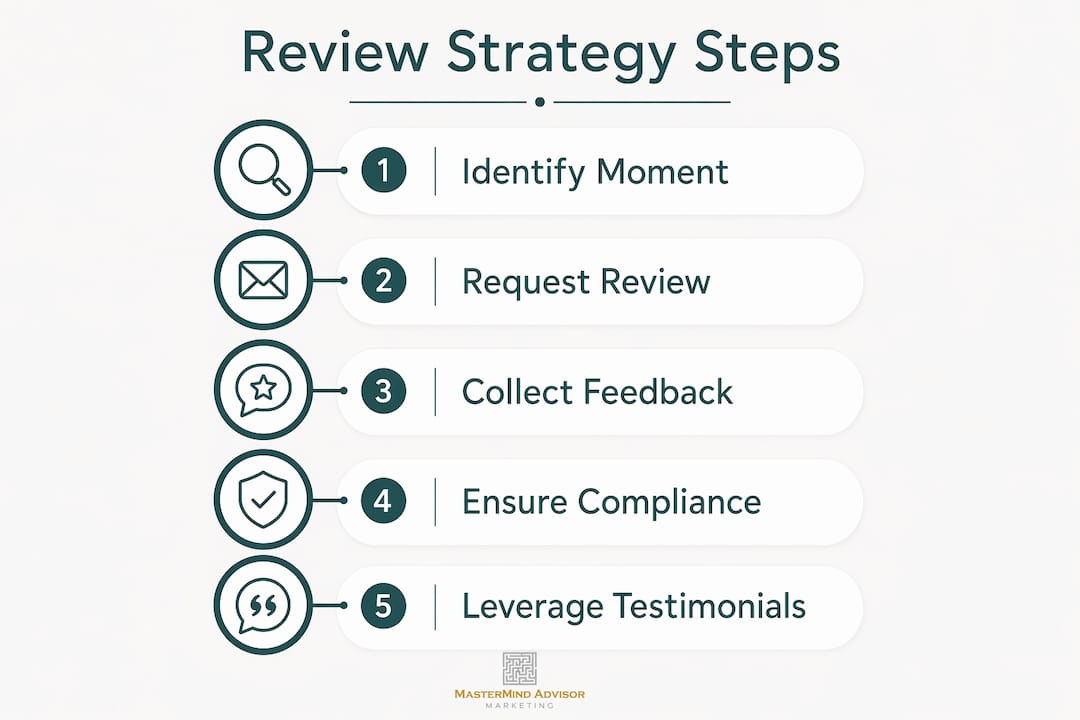

How to integrate a compliant review strategy into your workflow

The most effective approach embeds review requests into existing client service processes rather than treating them as separate marketing campaigns. Follow-up emails sent after meetings produce higher review collection rates than asking during the meeting itself. The client has time to reflect, the pressure is off, and the email provides a direct link that removes friction.

A practical workflow looks like this:

- Annual planning meeting: Conduct the review, summarize key decisions, and confirm the client feels heard.

- Follow-up email (24–48 hours later): Thank the client, recap the meeting's outcomes, and include a single, clear link to your preferred review platform.

- CRM automation: Log the request, set a 30-day reminder to check for a response, and archive the solicitation record for compliance purposes.

- Quarterly audit: Review your total review count, average rating, and response rate to identify gaps.

Review velocity matters more than volume. A steady flow of 10–12 new reviews per year outperforms a large batch of old reviews for both SEO and AI recommendation rankings. That means consistency beats intensity every time.

Pro Tip: Build your review request into your CRM as a standard post-meeting task, not an optional follow-up. When it lives in your workflow alongside meeting notes and action items, it gets done. When it lives in your intentions, it doesn't.

Compliance recordkeeping is non-negotiable. A compliant review program requires scalable supervision, dynamic disclosures tailored to each solicitation context, and full regulatory recordkeeping to avoid audit risk. Archive every request, every disclosure, and every response in a format your compliance team can retrieve quickly.

The 2026 digital marketing strategy for financial advisors increasingly treats review management as a core operational function, not a marketing add-on. Advisors who build that mindset now will find compliance audits and reputation management far less stressful.

What technology and compliance rules shape a modern review program?

The SEC Marketing Rule, which took full effect in 2021, permits advisors to use client testimonials and endorsements under specific conditions. Those conditions include clear disclosures, written agreements with compensated endorsers, and systematic recordkeeping. Multi-state advisors face additional complexity because state regulators may impose stricter requirements than the federal baseline.

AI-driven tools help manage review responses efficiently at scale, provide sentiment analysis across platforms, and flag compliance risks before they become violations. That operational consistency is difficult to achieve manually when you are managing dozens of client relationships simultaneously.

A well-designed technology stack for advisor review management typically covers four functions:

| Function | What it does |

|---|---|

| Automated solicitation tracking | Logs every review request with timestamp, client ID, and disclosure version |

| Lexicon screening | Scans incoming reviews for language that may trigger compliance concerns |

| Response management | Drafts and archives responses with human approval before posting |

| Sentiment monitoring | Tracks rating trends and flags sudden drops for immediate attention |

The human-in-the-loop step is critical. AI-driven tools can scale the monitoring and drafting functions, but a compliance-trained human must approve responses before they go live. Automating that final step creates regulatory exposure that no efficiency gain justifies.

Firms that treat review management as an integrated growth system benefit from operational efficiencies that manual processes cannot match. The technology does not replace judgment. It creates the conditions where good judgment can be applied consistently at scale.

Key Takeaways

A structured, compliant review strategy is the single most underdeveloped growth asset in independent financial advisory practices today.

| Point | Details |

|---|---|

| Reviews drive measurable growth | Advisors with review programs see 40–60% higher inbound conversion within 12–24 months. |

| Timing is everything | Request reviews after meetings via follow-up email to maximize response rates and preserve goodwill. |

| Compliance is non-negotiable | Archive every solicitation, disclosure, and response to meet SEC Marketing Rule requirements. |

| Velocity beats volume | A steady 10–12 new reviews per year outperforms old bulk reviews for SEO and AI rankings. |

| Early movers win | Only 10–15% of RIAs use testimonials actively, giving early adopters a clear competitive edge. |

What I've learned after watching advisors ignore this for too long

The most common thing I hear from advisors is that they feel awkward asking clients for reviews. I understand that instinct. The relationship feels too important to risk with what might seem like a self-serving request. But that framing is exactly backwards.

A review request, done well, is an act of service. You are giving a satisfied client the chance to help someone else find the guidance they need. You are also signaling that you care about your reputation and your practice's future. Clients who genuinely value you want to support you. Most of them just need to be asked.

What I have observed is that the advisors who resist review strategies are often the same ones who rely entirely on referrals and then wonder why their growth plateaus. Referrals are powerful, but they are invisible to the 25% of affluent prospects who now start their advisor search online. A practice with no digital review presence simply does not exist for that audience.

The shift I would encourage is moving from thinking about reviews as a marketing campaign to thinking about them as a client service standard. Every client deserves a relationship where their feedback is actively sought and genuinely used. When you build that culture, the reviews follow naturally. The client testimonial examples that resonate most are always the ones that sound like a real conversation, not a marketing script. That authenticity comes from advisors who ask because they care, not because they need content.

Technology makes the compliance side manageable. The mindset shift is the harder part, and it is the part that matters most.

— Josh

How Mastermindadvisormarketing supports your review strategy

Building a review program from scratch takes time you may not have. Mastermindadvisormarketing works exclusively with independent financial advisors to design and automate marketing systems that include review collection, CRM integration, and follow-up workflows built for compliance-conscious practices.

The platform's custom CRM tools and automated email sequences make it straightforward to embed review requests into your existing client service calendar without adding manual work. Advisors who use Mastermindadvisormarketing report stronger lead pipelines and more consistent client engagement across every stage of the relationship. If you are ready to build a review strategy that grows your practice and protects your reputation, visit Mastermindadvisormarketing to see how the system works for advisors like you.

FAQ

Why do financial advisors need a review strategy?

A review strategy builds the social proof that 83% of consumers require before hiring an advisor. It also improves search rankings and AI-based discovery, which increasingly drive new prospect inquiries.

When is the best time to ask a client for a review?

The best time is 24–48 hours after a high-value meeting, via a follow-up email with a direct link. Asking during the meeting itself produces lower response rates and can feel abrupt.

What compliance rules govern advisor testimonials?

The SEC Marketing Rule permits testimonials and endorsements with proper disclosures, written agreements for compensated endorsers, and systematic recordkeeping. Multi-state advisors must also check state-level requirements, which may be stricter.

How many new reviews does an advisor need each year?

A steady flow of 10–12 new reviews per year is more effective for SEO and AI rankings than a large batch of older reviews. Consistency signals an active, trusted practice to both search engines and prospects.

What is the biggest mistake advisors make with review programs?

The most common mistake is treating review collection as a one-time campaign rather than an ongoing client service standard. Advisors who ask once and stop see review velocity drop, which weakens their search presence and social proof over time.